Justice, Peace, Integrity

of Creation

Justice, Peace, Integrity

of Creation

By John Paul Pezzi, Mccj

Justice, Peace, Integrity

of Creation

By John Paul Pezzi, Mccj

Justice, Peace, Integrity

of Creation

By John Paul Pezzi, Mccj

Justice, Peace, Integrity

of Creation

By John Paul Pezzi, Mccj

In the silence, debt crushes fragile countries

Avvenire 27.06.2025 Paolo M. Alfieri Translated by: Jpic-jp.orgThe new UNCTAD report highlights that 3.4 billion people live in countries spending more on debt interest than on health or education. Yields on African ten-year bonds skyrocket.

While diplomacy speaks only of weapons, war, and defense, the silence surrounding development financing is becoming ever more deafening, despite the UN Conference on this issue opening these days in Seville, already marked by the announced absence of Trump’s USA. Virtually ignored by the media, the UN agency for trade and development (UNCTAD) released its annual report yesterday in New York with alarming new data on global debt, especially concerning developing countries, whose economies are being crushed by interest payments owed to private, public, and multilateral creditors.

In just one year, the report “A World of Debt” confirms, the total net interest on the debt of vulnerable countries increased by 10%, reaching $921 billion, with these countries being forced to borrow at increasingly higher rates on the global credit market. Overall, global debt has reached $104 trillion (up from $97 trillion in 2023), with one-third of this amount, $31 trillion, being the debt of developing countries. Over the past ten years, debt in fragile countries has grown at twice the rate of that in advanced economies.

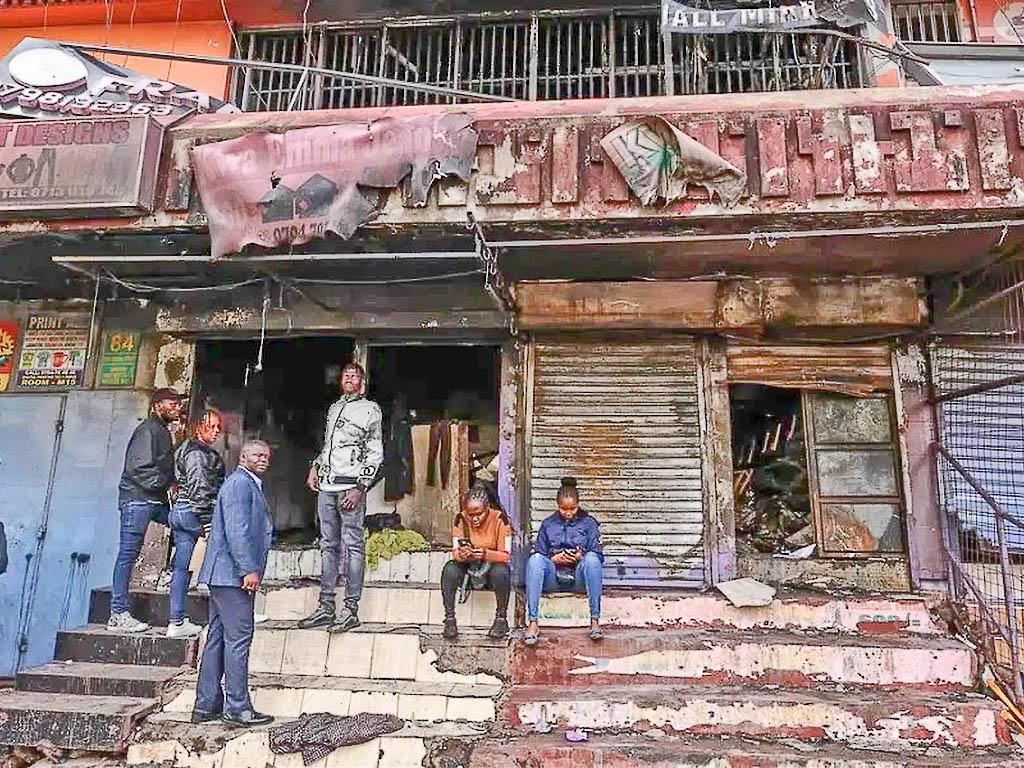

While global aid is collapsing — especially U.S. aid linked to the USAID program, but also aid from several European countries — fragile nations struggle to increase their tax revenues, due to the largely informal nature of their economies and the lack of transparency and adequate infrastructure. Now, UNCTAD points out, 3.4 billion people worldwide (up from 3.3 billion a year ago) live in countries forced to spend more on debt interest than on health or education. This affects 61 countries, compared to 54 last year. The result is that access to basic services remains a distant dream for a large portion of the global population, fuelling discontent in local communities and leading to violent street clashes, as recently seen in Kenya.

Developing countries have also experienced a net outflow of resources for the second consecutive year, repaying foreign creditors $25 billion more in debt servicing than they received in new disbursements, resulting in a negative net resource transfer. Moreover, the credit market offers no leniency to fragile states. Perceived as “riskier,” with little bargaining power, developing countries have seen their bond yields soar. An African ten-year bond yields on average 9.8%, UNCTAD reports, a Latin American bond 7.1%, and an Asia-Oceania bond 5.5%, compared to an average of 2.8% for a U.S. ten-year bond between 2020 and 2025. This means fragile states must offer higher returns to creditors just to secure fresh funds to keep functioning.

Debt restructurings, in cases of payment defaults by poor countries, have in recent years been marked by lengthy and difficult negotiations, partly because the credit market is increasingly dominated by private players, while there have already been 14 defaults in 9 different countries since 2020. In recent days, the Vatican Jubilee Commission, appointed by Pope Francis, has issued an appeal for the reform of the global financial architecture, so that it serves people and the planet and does not punish the poorest in the name of profit. To achieve this, the Commission suggests promoting sustainable development financing aimed at long-term socio-economic goals with concessional rates, and improving current debt restructuring policies by making them more timely, practical, and based on growth rather than mere austerity.

See, Nel silenzio il debito stritola i Paesi fragili: interessi a +10% in un anno

Photo. The remains of a burned shop in Nairobi, in recent days, during anti-government protests – Ansa

The comments from our readers (1)

The need for hope

Erich Fromm, in his book The Revolution of Hope, tells us that hope is paradoxical: “it is neither a passive waiting nor a violent forcing of realities that will not occur. [...]

The need for hope

Erich Fromm, in his book The Revolution of Hope, tells us that hope is paradoxical: “it is neither a passive waiting nor a violent forcing of realities that will not occur. [...]  In your previous book, Tiempo de cuidados (A Time for Care), you discussed the need to care for one another as a society. This new book seems to go a step further: if we are unable to care, we should [...]

In your previous book, Tiempo de cuidados (A Time for Care), you discussed the need to care for one another as a society. This new book seems to go a step further: if we are unable to care, we should [...]  Working over 80 hours a week. Unpaid. That was the call made by Elon Musk during his time as head of the U.S. Department of Government Efficiency, appealing to “revolutionaries with very high [...]

Working over 80 hours a week. Unpaid. That was the call made by Elon Musk during his time as head of the U.S. Department of Government Efficiency, appealing to “revolutionaries with very high [...]  In a ranch in Teuchitlán, a rural area an hour from the city of Guadalajara (and just half an hour from a military barracks), behind a gate like so many others in Mexico, the collective [...]

In a ranch in Teuchitlán, a rural area an hour from the city of Guadalajara (and just half an hour from a military barracks), behind a gate like so many others in Mexico, the collective [...]  The ‘new things’ of Pope Leo XIII's time are no longer so today in Europe, North America and certain regions of Asia, however they still are in several developing countries and even [...]

The ‘new things’ of Pope Leo XIII's time are no longer so today in Europe, North America and certain regions of Asia, however they still are in several developing countries and even [...]  A Christian drama is bread without solidarity. Let us take the theme of the communal table that touches the first centuries of Christianity. The table unites, in the memory of the supper, but also in [...]

A Christian drama is bread without solidarity. Let us take the theme of the communal table that touches the first centuries of Christianity. The table unites, in the memory of the supper, but also in [...]  Michiko Kakutani, wrote a book on, The death of truth: how we gave up on facts and ended up with Trump. In an article for The Guardian likens our times to Orwell's Ministry of Truth in Nineteen [...]

Michiko Kakutani, wrote a book on, The death of truth: how we gave up on facts and ended up with Trump. In an article for The Guardian likens our times to Orwell's Ministry of Truth in Nineteen [...]  Anti-Christian persecution keeps growing: the danger is increasing especially in Africa. Never so intense as in the last three decades. More than 365 million Christians experience a high level of [...]

Anti-Christian persecution keeps growing: the danger is increasing especially in Africa. Never so intense as in the last three decades. More than 365 million Christians experience a high level of [...]  A study carried out by scientists with groups of fish, the results of which they believe can be extrapolated to human societies, was published in the journal Science in 2011, under the title [...]

A study carried out by scientists with groups of fish, the results of which they believe can be extrapolated to human societies, was published in the journal Science in 2011, under the title [...]  The provocative motto recalls a famous phrase by Jean-Jacques Rousseau: “When the people have no more to eat, then they will eat the rich.” It is therefore clear on whose side those who [...]

The provocative motto recalls a famous phrase by Jean-Jacques Rousseau: “When the people have no more to eat, then they will eat the rich.” It is therefore clear on whose side those who [...] Info

Email: jampypezzi@gmail.com - tel. +39 328 732 6990 / +243 991 457 856

This blog is made in 4 languages: it en fr es

EDitt | Web Agency

EDitt | Web Agency

Leave a comment